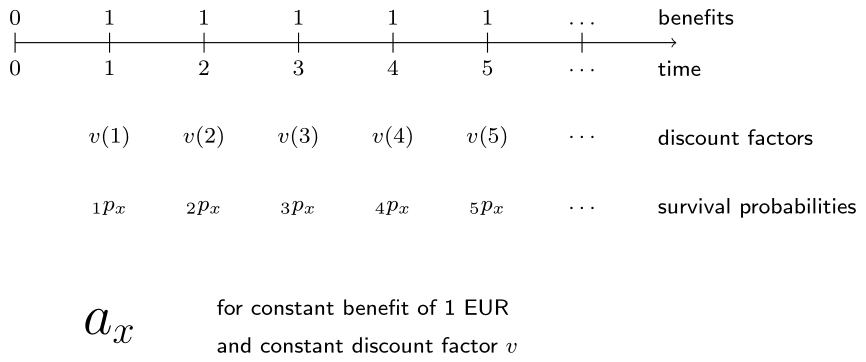

Sofort fällig vs vorschüssig

Als Anschlussaufgabe bittet Cynthias Vorgesetzte sie herauszufinden, wie das Skript für eine sofort beginnende Leibrente anzupassen ist, bei der die Zahlungen nach einem Jahr starten.

Die belgische Sterbetafel 1999 für Frauen ist als life_table vorab geladen, und der Lösungscode aus der vorherigen Übung dient als Ausgangspunkt. Tippe life_annuity_due in die Konsole, wenn du die Funktionsdefinition noch einmal ansehen möchtest.

Diese Übung ist Teil des Kurses

<Kurs>Bewertung von Lebensversicherungsprodukten in R</Kurs>Übungsanweisungen

- Lehn dich an die Funktion

life_annuity_due()an und schreibe eine neue Funktionlife_immediate_annuity(), die den BWZ (EPV) einer ganzen, sofort beginnenden Leibrente berechnet. Da es bei einer sofort beginnenden Rente zum Zeitpunkt 0 keine Zahlung gibt, sollen sowohlkpxals auchdiscount_factorsab Zeitpunkt 1 definiert werden. - Berechne den BWZ einer ganzen, sofort beginnenden Leibrente für (20) bei einem konstanten Zinssatz von 2 % mit

life_table. Überprüfe, dass das Ergebnis um 1 EUR niedriger ist als bei der vorschüssigen Rente.

Interaktive praktische Übung

Versuche dich an dieser Übung, indem du diesen Beispielcode vervollständigst.

# EPV of a whole life annuity due for (20) at interest rate 2% using life_table

life_annuity_due(20, 0.02, life_table)

# Function to compute the EPV of a whole life immediate annuity for a given age, interest rate i and life table

life_immediate_annuity <- function(age, i, life_table) {

px <- ___

kpx <- ___(px[(age + 1):length(px)])

discount_factors <- (___) ^ - (___)

sum(___)

}

# EPV of a whole life immediate annuity for (20) at interest rate 2% using life_table

life_immediate_annuity(___, ___, ___)